The fire-resistant coating market was USD 975 million in 2020 and is projected to reach USD 1,125 million by 2026, at a CAGR of 3.5%. Europe accounted for the largest share of the market. It is projected to reach USD 490 million by 2026, at a CAGR of 3.0%, between 2021 and 2026. The growing building & construction sector in the region is projected to drive the market. Due to stringent government regulations and fire safety norms in developed regions, fire-resistant coatings have become an indispensable part of the buildings & construction industry as well as the oil & gas, chemical, and other industries wherein the chances of fire hazards are high.

The fire-resistant coating is applied to surfaces to protect them against fire and to reduce the loss incurred due to fire hazards in buildings & construction as well as in the manufacturing sector. Industrially, intumescent coating and cementitious coatings are applied on the surface of steel, wood, plastics, and other materials to evade the propagation of fire and to maintain structural integrity by resisting fire, which, in turn, helps to save lives and minimize the damage. The selection of fire-resistant coatings depends on construction types, fire safety norms, international building standards and regulations, and potential fire. These coatings are used in commercial and residential buildings and industrial applications. They are also used for exterior and interior steel applications, walls, and steel frameworks.

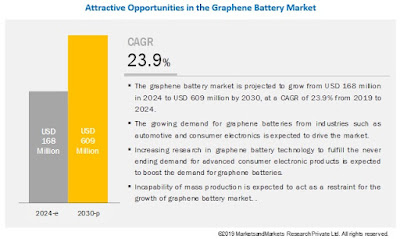

To know about the assumptions considered for the study download the pdf brochure

The leading players in the fire-resistant coating market include Akzo Nobel (Netherlands), PPG (US), Jotun (Norway), Sherwin-Williams (US), and Hempel (Denmark). The key industry players are adopting strategies to expand their presence and enhance their product portfolio through investments in R&D.

Due to the rise in the number of fire accidents at residential, public places, and workplaces, the number of deaths and damage to assets is also increasing. In view of this, end-users are increasingly adopting safety measures to protect people and property. Governmental agencies are also making rules regarding the addition of fire-resistant coatings in buildings to reduce these fire accidents.

AkzoNobel N.V., AkzoNobel is engaged in the manufacturing and sales of paint and coating products. It operates its business through two major segments⎯Decorative Coatings and Performance Coatings. The company has over 28 manufacturing facilities and has sales activities in more than 150 countries across the globe. The Performance Coatings segment is divided into marine and protective coatings, automotive and specialty coatings, industrial coatings, and powder coatings. Under the protective coatings sub-segment, the company offers intumescent coating products, i.e., passive fire resistance coating products under the trademarks “Interchar” and “Chartek.” The company offers 23 types of passive fire protection coatings products for building & construction, oil & gas, and other industrial applications.

PPG Industries, Inc., PPG Industries is a global supplier of paints, coatings, optical products, and specialty materials. It serves customers in industrial, consumer products, transportation, and construction markets. PPG has headquarters in Pittsburgh. The company has 156 manufacturing facilities worldwide. It caters to North America, South America, Asia Pacific, Europe, the Middle East, and Africa. The company has two major segments: Performance Coatings and Industrial Coatings. Performance coating is further segmented into Automotive Refinish Coatings, Aerospace Coatings, Protective and Marine Coatings, and Architectural Coatings. Fire-resistant coating comes under the Protective and Marine Coatings segment.

Companies have initiated the following developments:

- In May 2020, Hempel A/s has begun the construction of a new factory in Yantai Chemical Industrial Park, China. The plant will have a production capacity of more than 100,000 tons per year and will be inaugurated by 2021.

- In December 2019, The Sherwin-Williams Company announced the opening of a new 4,200-square-feet store in Alexandria Bay, New York, US.

- In July 2019, The Sherwin-Williams Company opened a new store in Florida, US.

- In September 2020, Etex Group had acquired the UK-based passive fire protection company named FSi Limited, having a production facility in Measham, East Midlands, and a distribution center in London.

- In August 2019, the Sherwin-Williams Company acquired the business and assets of Dresdner Lackfabrik Novatic (Germany) in Germany, Poland, and the Czech Republic.

- In May 2019, Teknos Group acquired the Czech Republic-based Finnproduct, a distributor, to expand its customer base to the domestic market

- In March 2019, AkzoNobel N.V. launched a new fire protection coating system for the wooden building façade, which got approved in Europe.

- In February 2020, Teknos Group launched intumescent paint, “TEKNOSAFE 2407,” for the building and construction industry.