The report “Hydrogel Market by Raw Material Type (Natural, Synthetic, Hybrid), Composition (Polyacrylate, Polyacrylamide, Silicon), Form (Amorphous, Semi-crystalline, Crystalline), Application (Contact Lens, Personal Care & Hygiene), Region – Global Forecast to 2022″, The hydrogel market is estimated to be USD 11.43 Billion in 2017 and is projected to reach USD 15.33 Billion by 2022, at a CAGR of 6.04% between 2017 and 2022. The growth of the hydrogel market can be attributed to an increase in the consumption of personal care & hygiene products in emerging economies and a rise in the production facilities of hydrogels.

Browse 80 Market Data Tables and 31 Figures spread through 133 Pages and in-depth TOC on “Hydrogel Market”

The agriculture segment is projected to grow at the highest CAGR during the forecast period

Based on application, the agriculture segment is anticipated to grow at the highest CAGR during the forecast period. This growth can be attributed to the increasing agricultural activities in various regions, such as Asia Pacific, North America, Europe, and the Middle East & Africa. Moreover, the growing usage of hydrogels as a key material for farming, owing to its characteristics such as water holding ability, has contributed to the growth of the hydrogel market in agriculture.

The polyacrylate segment is projected to be the fastest-growing composition segment of the hydrogel market

Based on composition, the polyacrylate segment of the hydrogel market is anticipated to grow at the highest CAGR between 2017 and 2022. This growth can be attributed to the water retention ability of polyacrylate hydrogels that increase their applicability in the personal care & hygiene application. Moreover, superior properties of hydrogels, such as transparency and elasticity, have further led to the growth of the polyacrylate segment.

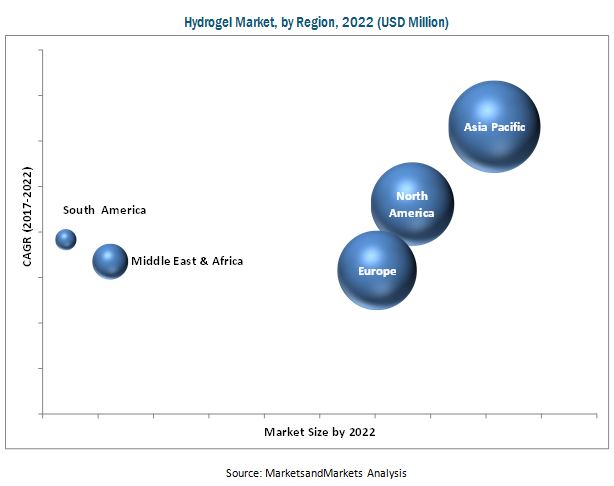

The hydrogel market in the Asia Pacific region is projected to grow at the highest CAGR during the forecast period

Asia Pacific accounted for the largest share of the hydrogel market in 2016. This market in the Asia Pacific region is projected to grow at the highest CAGR from 2017 to 2022. Among all countries in the Asia Pacific region, the hydrogel market in India is projected to grow at the highest CAGR during the forecast period. This market in North America is projected to grow at the second-highest CAGR between 2017 and 2022, with the US registering the highest growth rate in this region.

Key players operating in the hydrogel market include Johnson & Johnson (US), Cardinal Health (US), the 3M Company (US), Coloplast (Denmark), B. Braun Melsungen (Germany), Smith & Nephew (UK), Derma Sciences (US), Royal DSM (Netherlands), Dow Corning Corporation (US), Paul Hartmann (Germany), Momentive Performance Materials (US), Ocular Therapeutix (US), ConvaTec (UK), Ashland (US), Evonik Industries (Germany), Cosmo Bio USA (US), MPM Medical (US), Molnlycke Health Care (Sweden), Hollister (US), Medline Industries (US), Gentell (US), and Alliqua BioMedical (US). These players have adopted various growth strategies to expand their global presence and increase their market share. Mergers & acquisitions, expansions, and new product launches are some of the major strategies adopted by key players operating in the hydrogel market.