To know about the assumptions considered for the study download the pdf brochure

Chlor-alkali products such as chlorine, caustic soda, and soda ash play a vital role in the chemical industry. These products are necessary raw materials in major bulk chemical industries and utilized in various industrial and manufacturing value chains. The products are used in different applications such as plastics, alumina, paper & pulp, and others and find applications in diverse end-use industries (construction, automotive, and others). Thus, rising chemical output and strong economic conditions in emerging countries are expected to drive the growth of the chlor-alkali market.

- According to the European Chemical Industry Council (Cefic), in 2019, the global sale of chemicals was worth USD 4,108 billion. China dominates the sales of chemicals, followed by the European Union and the US. The sales of chemicals are expected to reach USD 6.9 trillion by 2030. Chlor-alkali products being one of the key raw materials for various products in the chemical industry, high demand is expected to further drive demand.

- According to PlasticsEurope, global plastic production in 2019 was 368 million tons. APAC dominated the market accounting for 51% of the global production.

- PVC is utilized in the construction, electronics, healthcare, automotive, packaging, and other end-use industries. Its low cost and desirable physical & mechanical properties make it a suitable material was various applications. In 2019, the demand for PVC in Europe was approximately five million tons, which accounted for 10% of the overall production of plastic in Europe.

- There is high growth in the construction sector in the US, China, and India. In 2019, the contribution of construction to the GDP of India, the US, and China was approximately 9%, 6%, and 7% respectively.

- Recovery of the automotive sector is expected to drive the demand for PVC, aluminum, and other materials in the automotive industry which is expected to further drive the market for chlor-alkali products

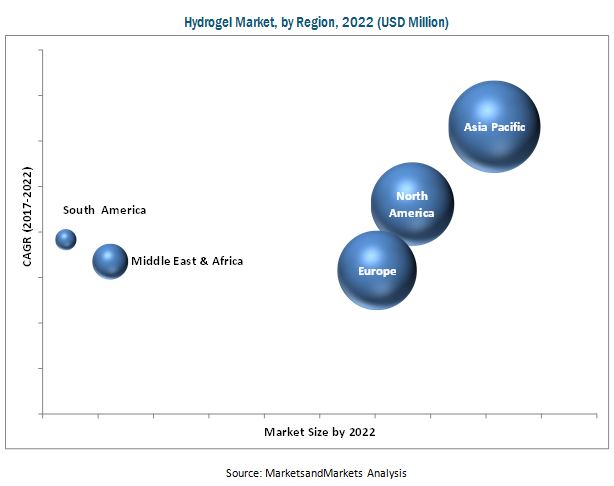

APAC accounted for the largest share of the Chlor-Alkali market in 2020, followed by Europe and North America. APAC recorded the largest demand for chlor-alkali in the past few years due to the growing investments in developing countries and manufacturing capacity additions across end-use industries, especially water treatment, and chemical processing. Increasing investments in infrastructure development projects, growing urbanization, rapid industrialization, improving the standard of living, and thriving automotive sector, as well as high economic growth, are the key factors for the regions overall growth.

The leading players in the Chlor-Alkali market are Olin Corporation(US), Westlake Chemical Corporation (US), Tata Chemicals Limited (India), Occidental Petroleum Corporation (US), Formosa Plastics Corporation (Taiwan), Solvay SA (Belgium), Tosoh Corporation (Japan), Hanwha Solutions Corporation (South Korea), Nirma Limited (India), AGC, Inc. (Japan), Dow Inc. (US), Xinjiang Zhongtai Chemical Co. Ltd. (China), INOVYN (UK), Ciner Resources Corporation (US), Wanhua-Borsodchem (Hungary), and others.

Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=708

The leading players in the Chlor-Alkali market are Olin Corporation(US), Westlake Chemical Corporation (US), Tata Chemicals Limited (India), Occidental Petroleum Corporation (US), Formosa Plastics Corporation (Taiwan), Solvay SA (Belgium), Tosoh Corporation (Japan), Hanwha Solutions Corporation (South Korea), Nirma Limited (India), AGC, Inc. (Japan), Dow Inc. (US), Xinjiang Zhongtai Chemical Co. Ltd. (China), INOVYN (UK), Ciner Resources Corporation (US), Wanhua-Borsodchem (Hungary), and others.

Request for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=708